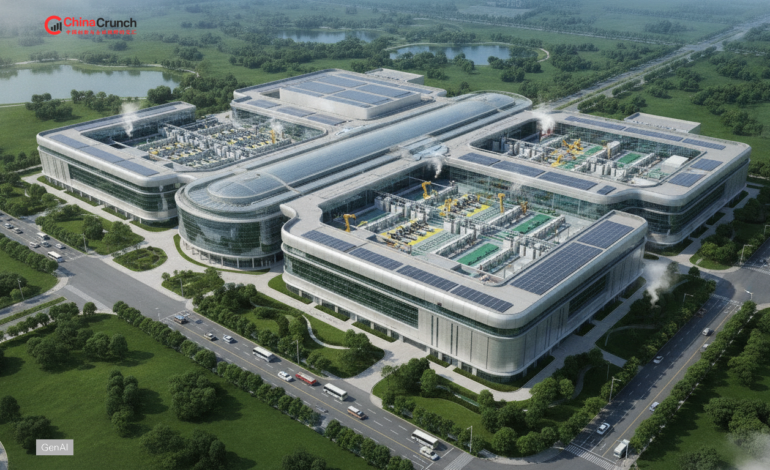

China semiconductor industry gains momentum on stability

China semiconductor industry outlook and policy stability

The China semiconductor industry is being shaped by what many executives and long time investors describe as clearer policy signals and a stronger focus on predictable execution. Business confidence has been influenced by senior executives and long time investors who cite stability as a factor in long cycle projects like fabs, packaging plants, and design programs. In boardrooms, the sector is often assessed as a portfolio of manufacturing, packaging, and design capabilities that can keep operating through demand cycles. Corporate counsel also notes that clearer compliance expectations can reduce project delays, while investors focus on governance, power availability, and permitting speed that can affect utilization and output reliability.

Investment, demand drivers, and capacity build in China

Capital spending decisions increasingly track adjacent buyers of chips, including electric vehicles, industrial automation, and consumer devices. Demand for AI infrastructure is also pulling spending forward: the South China Morning Post reported that ByteDance is spending billions on AI (ByteDance spends billions on AI and chip start ups), spotlighting which domestic chip start ups could benefit in accelerators, memory, and networking. Investors also watch financing channels and project pipelines tied to energy and logistics, including China-Pakistan trade shifts amid EU policy pressure, as companies reportedly diversify invoicing hubs and supply routes, and procurement teams factor in changing payment and shipping constraints.

Mature nodes, packaging, and global market effects

Domestic output plans can influence pricing and allocation across mature process nodes used in autos, power management, and industrial control, according to market participants. In the China semiconductor industry, when domestic fabs expand in these segments, overseas suppliers may respond by shifting wafers toward specialty products with higher margins, as industry observers often note. The sector also affects packaging and test because more local assembly can change where value is captured and how quickly products move from wafer to shipment. Upstream components like PCBs matter as well, especially where capacity additions may signal broader electronics demand, as covered in China tech startups watch Kingboard PCB capacity boost, and buyers continue spreading orders to reduce single region exposure, according to procurement teams.

Export controls, tooling access, and operational constraints

Operational risk remains concentrated around tooling access, verification software, and the availability of certain advanced materials, according to companies managing cross border supply chains. As indicated by companies, restrictions introduced by the United States and expanded in October 2022 and October 2023 reportedly tightened access to advanced computing chips and certain semiconductor manufacturing equipment, which can lengthen qualification cycles for substitutes and increase compliance work. Yield learning remains a slower constraint than new buildings in many fabs, as engineers often emphasize that defect density, metrology cadence, and process control determine whether added capacity becomes shippable dies. A structural lens on AI and the chip supply chain is also discussed by the South China Morning Post (US AI dominance vulnerable to China amid structural challenges), and these pressures have reportedly pushed firms to strengthen documentation and vendor auditing.

What to watch next for China semiconductor industry growth

Near term momentum depends on whether capital, talent, and customer demand stay aligned across design, manufacturing, and systems integration, according to investors tracking the sector. Large semiconductor projects typically require multi year execution, and lenders generally want predictable rules on land use, energy contracts, and cross border payments. Within the China semiconductor industry, growth is expected by analysts to cluster where China already has scale, including power devices, sensors, display drivers, and advanced packaging that can lift performance without relying on the smallest lithography steps. IPO and funding pathways for AI related chip ecosystems are also evolving, including Shanghai’s moves to open IPO access for some cash hungry AI labs (Shanghai charts IPO path for AI labs), as reported by the South China Morning Post. Market impact will likely hinge on how quickly new capacity is absorbed by real orders rather than inventory.