Humanoid robots in China: fast track to factory use

Humanoid robots in China: nationwide factory pilots

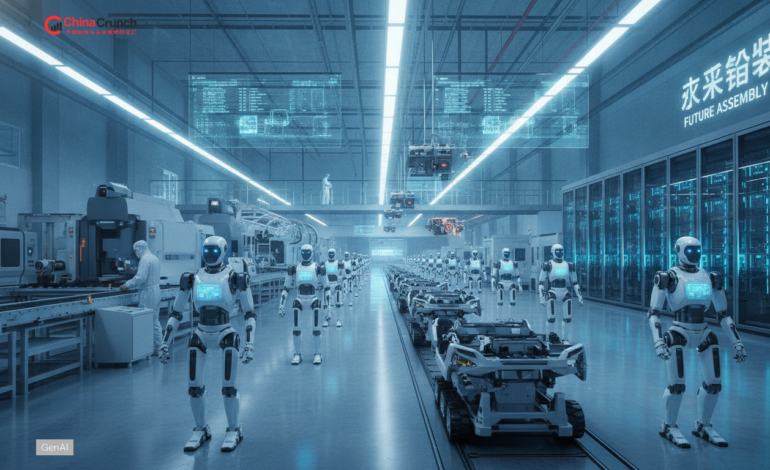

China appears to be moving from lab demos to more coordinated factory trials as ministries and local governments signal interest in procurement, testing standards, and industrial parks for embodied systems. In these deployments, humanoid robots in China are being positioned by some vendors and plant partners as general-purpose workers that can traverse existing shop floors without rebuilding every line. The Ministry of Industry and Information Technology (MIIT) has described humanoid development as a priority within its robotics and intelligent manufacturing agenda, with public communications emphasizing reliability and safety goals. In several provinces, local programs are reportedly pairing manufacturers with robotics firms to validate material handling and inspection under real shift conditions. Operators typically want hard numbers on uptime, fault recovery, and safe stops before broader rollout, according to industry participants.

Industrial roles and deployment targets

Factory managers in China are prioritizing use cases where a legged or wheeled biped can switch between workstations designed for humans, potentially reducing retrofit time for robot automation. In automotive and electronics plants, integrators are reportedly testing pick-and-place, bin sorting, and tool handoffs where dexterous end effectors matter more than maximum payload. Line engineers generally map tasks to cycle time targets, safety zones, and operator handoff points before expanding deployments beyond pilots, and for regional context on broader infrastructure coordination, see China Pakistan Economic Corridor: projects and trade. For related industrial investment context, see China EV industry investment revives Europe car factories in assessments of manufacturing-linked capital flows.

Embodied AI advances and hard factory constraints

Many of the reported gains come from tighter coupling between perception, planning, and actuation, an approach vendors describe as embodied AI trained on factory constraints rather than generic internet data. Teams are increasingly training on structured datasets from warehouses and mock production cells, then validating against repeatability, collision avoidance, and emergency stop requirements, according to company briefings and demo materials. Hardware groups in China are also working to localize key components such as harmonic drives, torque sensors, and force-controlled joints to reduce supply risk, as industry participants have stated in public interviews and product notes. Compute availability and model governance can still shape rollout pace, especially when plants require on-premises inference and detailed logging for every shift, and for background on data policy and training capacity, see China’s Evolving AI Data Strategy to Mitigate Training Shortages. For silicon constraints and deployment planning, see Huawei AI chips: Ascend 910C specs and DeepSeek use in discussions of hardware roadmaps.

Policy support, standards, and procurement

Policy support is being discussed in terms of testbeds, certification pathways, and purchase incentives that could lower early adopter risk for AI in industry, though details vary by locality and program. MIIT has emphasized standard setting for robots, including interoperability and safety, in its public messaging around scaling intelligent manufacturing. Local governments are also reportedly funding shared facilities where firms can benchmark locomotion, dexterity, and battery endurance under identical protocols. Manufacturers frequently ask for clearer liability rules for human-robot collaboration, while regulators tend to emphasize auditability for models that make motion decisions. Procurement departments are beginning to draft requirements around mean time between failures, remote diagnostics, and maintenance training tied to documented service intervals, according to integrators and plant-side procurement discussions in Guangdong and Zhejiang. The near-term trajectory appears to favor controlled expansion in logistics, 3C assembly support, and hazardous inspection rather than fully autonomous line replacement.

Global market impact and export readiness

China’s acceleration could reshape competitive dynamics if suppliers continue bundling actuators, sensors, and controllers into standardized stacks aimed at export-ready industrial packages. If domestic scale lowers component costs and shortens iteration cycles, pricing pressure may rise in sectors already dominated by Chinese manufacturing, though outcomes depend on sustained field performance. International buyers will still evaluate cybersecurity, certification, and spare parts availability before adopting a new class of worker, and South China Morning Post has tracked governance risks that firms cite when hardening industrial models in coverage of China sounds alarm over AI ‘skills’ that evade guard rails and mine crypto. Rival ecosystems in the United States, Japan, and Europe are likely to respond with tighter safety frameworks and niche specialization, as analysts often forecast. Market impact ultimately hinges on whether pilots translate into stable utilization rates across multiple factories and seasons for humanoid robots in China.